El dólar estadounidense experimentó un desempeño volátil la semana pasada, donde todos los ojos estaban puestos en la Reserva Federal. El banco central cumplió, elevando las tasas de interés de los préstamos de referencia en 50 puntos básicos. La reacción inicial fue una subida moderada, ya que el presidente de la Fed, Jerome Powell, restó importancia a las expectativas de subidas de tipos de 75 puntos básicos que los mercados estaban considerando en los próximos meses. Como resultado, el dólar bajó.

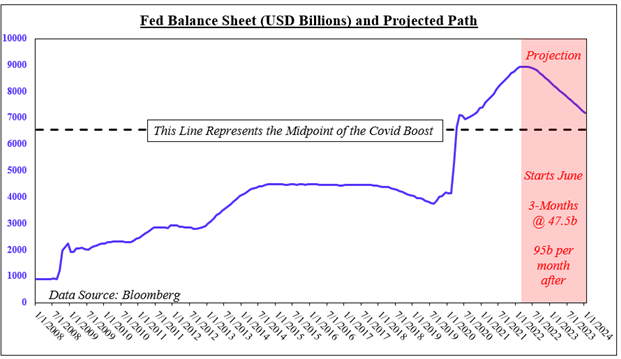

A medida que los operadores dirigieron la información, el sentimiento cambió de rumbo y el dólar estadounidense recuperó su equilibrio. Al final del día, el ajuste cuantitativo está a la vuelta de la esquina. En el cuadro a continuación se muestra cómo podría verse esto. Comenzando a un ritmo inicial de USD 47,500 millones por mes en junio, acelerando hasta 95b 3 meses después, el tamaño del balance aún sería superior al punto medio del impulso de Covid para 2024.

Datos del mercado laboral de EE. UU.

En la próxima semana, el dólar estadounidense estará pendiente del próximo informe de inflación estadounidense del 11 de mayo . Se espera que la inflación general se enfríe al 8,1 % a/a en abril desde el 8,5 % anterior. Esto se debe a que el IPC básico se prevé en 6,1% desde el 6,5% anterior. Si bien esto representaría cierta desinflación, se mantiene muy por encima del objetivo del banco central. Un informe más sólido podría impulsar aún más al dólar estadounidense y amplificar la aversión al riesgo.

Interesante, mirando el índice de sorpresa económica de Citi, los datos de EE. UU. todavía tienden a superar las expectativas de los economistas. Sin embargo, el margen de resultados halagüeños en relación con las estimaciones se ha ido reduciendo. Hubo un máximo de 70 en abril antes de caer a 18 antes del informe de

nóminas no agrícolas. Los valores por debajo de 0 representan resultados cada vez más suaves en relación con el consenso.

Una gran cantidad de Fedspeak también cruzará los cables. Estos incluyen a Loretta Mester, Raphael Bostic y John Williams, presidentes de las sucursales de Cleveland, Atlanta y Nueva York, respectivamente. Hasta cierto punto, podrían infundir confianza en que la economía sea capaz de soportar un endurecimiento monetario agresivo. Esto podría ofrecer un alivio a corto plazo para el sentimiento, quizás amenazando al dólar estadounidense.

Sin embargo, considerando todas las cosas, el dólar aún permanece en una posición para continuar actualizándose frente a sus principales pares. Podría decirse que el banco central sigue siendo el más agresivo entre sus homólogos del G-10. Mientras tanto, el balance estancado sigue siendo un obstáculo para que la confianza cambie sustancialmente de rumbo. Por lo tanto, es una llamada alcista para la moneda de reserva mundial esta próxima semana.

Datos del mercado laboral de EE. UU.

US dollar and its approach

The US dollar saw a volatile performance last week when all eyes were on the Federal Reserve. The central bank complied, raising benchmark lending rates by 50 basis points. The initial reaction was a moderate hike as Fed Chairman Jerome Powell downplayed expectations of 75 basis point rate hikes that markets were eyeing in the coming months. As a result, the dollar fell.

As traders led the data, sentiment turned around and the US dollar regained its footing. At the end of the day, quantitative tightening is just around the corner. The chart below shows how this might look. Starting at an initial pace of $47.5bn per month in June, accelerating to 95b 3 months later, the size of the balance sheet would still be above the midpoint of the Covid momentum by 2024.

What is the balance sheet supposed to look like when 2024 begins?

In the coming week, the US dollar will be watching the next US inflation report on May 11th. Headline inflation is expected to cool to 8.1% y/y in April from 8.5% previously. This is because the core CPI is forecast at 6.1% from 6.5% previously. While this would represent some disinflation, it remains well above the central bank’s target. A stronger report could further boost the US dollar and amplify risk aversion.

Interestingly, looking at the Citi Economic Surprise Index, the US data still tends to beat economists’ expectations. However, the margin of encouraging results about the estimates has been shrinking. There was a high of 70 in April before falling to 18 before the report of non-farm payrolls. Values below 0 represent increasingly softer results relative to the consensus.

A lot of Fedspeak will also cross the wires. These include Loretta Mester, Raphael Bostic, and John Williams, presidents of the Cleveland, Atlanta, and New York branches, respectively. To some extent, they could instill confidence that the economy is capable of withstanding aggressive monetary tightening. This could offer short-term relief for sentiment, perhaps threatening the US dollar.

However, all things considered, the dollar remains in a position to continue to rally against its major peers. Arguably, the central bank remains the most aggressive among its G10 counterparts. Meanwhile, the stagnant balance sheet remains an obstacle for confidence to substantially change the course. Therefore, it is a bullish call for the global reserve currency this coming week.

US labor market data